2026

NOTE: There will not be a township workshop held in 2026.

Documents for the 2026 Annual Meeting:

- 2026 Hand County Auditor’s Newsletter for the Township Clerks

- Certification of Township Mileage for non-property taxes.

- Each year the Department of Legislative Audit examines these mileage reports. They are very important so that a township gets the right share of the taxes for road purposes.

- PT-73 Report detailing towns & townships valuations, levies, requests and expected returns for 2026.

- For the general levy, this will show you your new “base” or “general” levy to build the 2027 request from.

- Clerk’s Certification & Notice to the Auditor.

- Slight changes are present in the township mileage section. Please review ahead of time.

- Clerk’s report of township officers.

- Slight change. The clerk can place N/C (no change) in address, telephone and email address lines if there is no change.

- Township property tax OPT OUT resolution.

- The 2026 OPT OUT document from the Department of Revenue is not available as of 01/23/2026. Here is the 2025 pay 2026 link.

- OATH of office for both the township clerk and treasurer.

2025

On December 12, 2024, a letter was sent out to all 39 township clerks. The letter contained the information found in items 1 & 2. The content after that is general information. Check back often, more will be added as it becomes available.

Township Clerks – preparing for 2025 meetings and levy decisions:

- The 2025 base / general levy decisions are based on the amount of taxes requested the prior year. This file contains the levies approved by the SD-Department of Revenue. Click Pay 2025 All Districts (excluding schools) Property Taxes (you’ll see the County, Cities, Townships, Secondary Roads, Fire District)

- The base levy can be increased by the CPI (Consumer Price Index) and the grown within the district. The total of these two increases is then applied to the existing (current) request as shown in dollars.

- For example: If Township X requested $5,000 in the current year, the levy for the following year is:

- $5,000 times (CPI & Growth percentages) 3.05% (for this illustration) which equals $153.

- $5,000 * 3.05% = $153.00

- $5,000 + $153.00 = $5,153.00 for the new base / general request.

- The percentage of growth & cpi is not applied to the mill levy, only the monetary request.

- $5,000 times (CPI & Growth percentages) 3.05% (for this illustration) which equals $153.

- The CPI for taxes payable in 2026 is 2.9%.

- In December 2024 the SD-Department of Revenue made it clear they will not validate levy requests which are not clearly illustrated in the minutes of the annual meeting. This means that township supervisor boards (Chairman, Supervisor 1 and Supervisor 2) must move, second and pass a levy request for:

- The Base / General levy (decided by the 3 supervisors)

- A resolution to support a Secondary Road and Bridge Levy (eligible voters present at the annual meeting may vote)

- To use any portion of an existing opt out (no publication is needed for an existing opt out to be used)

- A resolution to support a new, non-preexisting opt out (which must be published)

The levy setting portion of your minutes might look as follows:

- It was moved by John Doe, seconded by JQ Public, passed, to apply the CPI and any growth to the current year’s levy amount of $5,213. This would be $5,213 + the percentage of CPI & growth.

- It was moved by JQ Public, seconded by John Doe, passed, to use $5,000 of the existing opt out authority.

- It was moved by John Doe, seconded by JQ Public, passed, to adopt resolution 2025.01 implementing an additional opt out (see separate, attached, resolution) for an additional $5,000 per year for the next 10 years.

- It was moved by John Doe, Seconded by JQ Public, passed by majority of eligible voters present, to impose a Secondary Road levy in the amount of 10,000 for taxes payable in 2026.

By clearly defining the use of each property tax levy, there should be no question as to the supervisor’s intent on what to levy upon the properties in the township.

It is also very important that township report their mileage accurately. This mileage report is used when dividing up / apportioning motor vehicle, fuel taxes and dealer fees. The miles reported need to meet statutory requirements for inclusion. This would be full maintenance and minimum maintenance roads (that should have appropriate signage). Unimproved roadways or roadways maintained by others should not be counted. Great care should be taken when reporting boarder roadways so that the two districts sharing the roadway only report their actual responsibility.

The Hand County Assessor’s Office and the Auditor’s Office will again be hosting a “township workshop” for Hand County township Clerks and Treasurers. Supervisors may also attend should they wish. The current plan is to hold this workshop somewhere in the first two full weeks of February ahead of your annual February meeting where you prepare for the Annual Meeting on March 4, 2025.

Township Clerks can download their forms from the 2024 information. As things change, I will update the forms as needed.

- Combined Oaths (Clerk and Treasurer) and Board Members report form.

- Combined Clerks Certification and Levy Request for the county auditor.

- Township “road and bridge” levy information and resolution form.

- South Dakota Department of Revenue webpage on OPT OUTs for (non-school) local governments.

- The pre-printed / pre-formatted opt out resolutions on pages 6 and 7. Be sure to note the difference between the two forms.

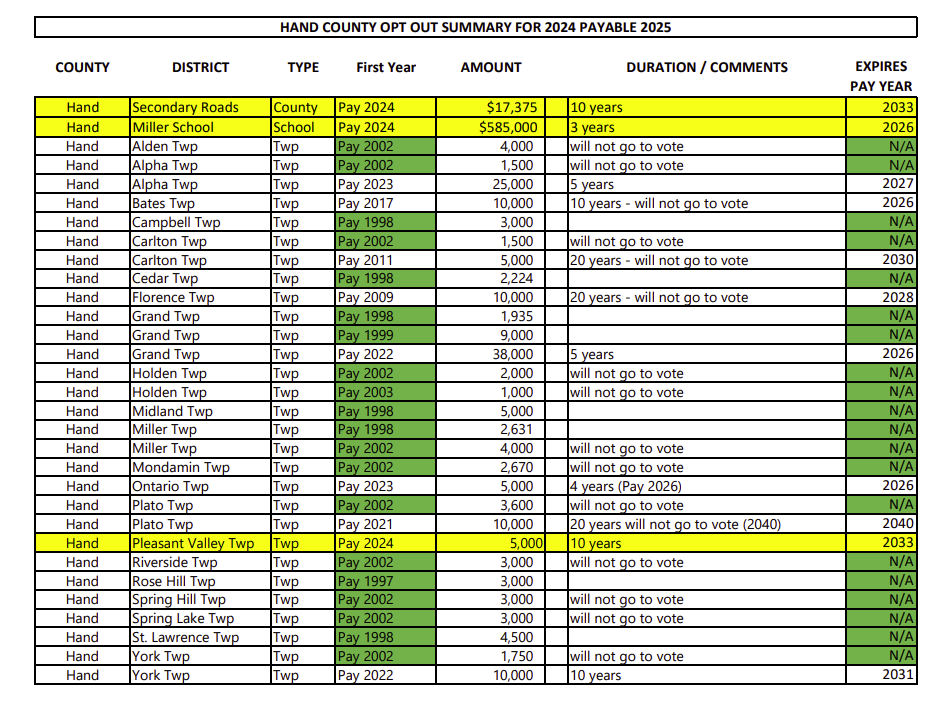

- List of Opt-Outs on record with the Department of Revenue:

- Summary of Opt-Outs for Townships as of March 2024 (ignore the school data)

- Yellow entries are 2023 payable 2024 opt out levies.

- Green entries are opt-outs between 1996 and 2003 which have no expiration data.

- Uncolored entries are opt-outs after 2003 which are currently valid.

- There were no new opt-outs inacted in 2024 for pay 2025.

- Several townships elected not to request their opt-out dollars but used the road and bridge levy instead.

- Summary of Opt-Outs for Townships as of March 2024 (ignore the school data)

2024

Township Clerks can download their forms from the 2024 information. As things change, I will update the forms as needed.

- Combined Oaths (Clerk and Treasurer) and Board Members report form.

- Combined Clerks Certification and Levy Request for the county auditor.

- Township “road and bridge” levy information and resolution form.

- South Dakota Department of Revenue webpage on OPT OUTs for (non-school) local governments.

- The pre-printed / pre-formatted opt out resolutions on pages 6 and 7. Be sure to note the difference between the two forms.

- 2023 payable 2024 Property Tax Summary report.

- This is where you find out what your base levy (dollar amount) is now and that is the number you can add the CPI factor to.

- The Road & Bridge Levy is requested as a mill-levy up to $0.50 / thousand.

- The OPT – OUT Levy is requested as a dollar amount up to the limit set in your current (active) resolution.

- South Dakota Department of Revenue “Consumer Price Index for 2024 – Taxes Payable 2025”

- A township may increase its “base” or general levy by the amount of the CPI without having to opt-out.

- For example, If “Township A” levied $5,500 to be collected in 2024 for the “base” or general levy, their new base / general levy would be: $5,500 * 3% ($165.00) for a new base / general levy of $5,665.00.

- The CPI only impacts the base/general levy and is applied to the dollar amount, not the mill levy. The CPI is not applicable to any opt out or road & bridge levy. The opt-out is a dollar amount up to the maximum authorized in the opt-out resolution and the road & bridge levy is a mill levy stated in cents per thousand, up to fifty cents.

- List of Opt-Outs on record with the Department of Revenue:

- Summary of Opt-Outs for Townships as of March 2024 (ignore the school data)

- Yellow entries are 2023 payable 2024 opt out levies.

- Green entries are opt-outs between 1996 and 2003 which have no expiration data.

- Uncolored entries are opt-outs after 2003 which are currently valid.

- Summary of Opt-Outs for Townships as of March 2024 (ignore the school data)

- MINUTES (They are extremely important)

- For each type of levy your township utilizes, a separate notation should be in your minutes. I suggest a paragraph for the general (base) levy, a paragraph of the opt-out levy and a paragraph for the resolution (in full text) for the road and bridge levy.

2024 values and growth to calculate the 2025 payable “BASE / General taxes”.

This link will provide you with a report produced from the SD-DOR property tax portal from data submitted by the assessor and later the auditor. You can use this information to calculate your township’s property base or general taxes. It doesn’t pertain to opt-outs which are limited to a fixed dollar amount set by the township board of supervisors. It also does not pertain to the road and bridge levy as that too is set by the township board of supervisors and only during the annual meeting.

Steps, using Alden Township as the illustration.

- Combine the state’s CPI percentage (3% in 2024) and the township’s growth percentage (0.05%) to get 3.05%.

- This 3.05% is the amount a district can raise their levy (in dollars) without having to opt-out of the tax limitations.

- From the report (linked above), use the total value of property, in this example, that is $38,286,484, as it will be need in the formula later.

- Using the link above, from the March meeting, locate your township’s levy amount (in dollars), in this case, the general / base levy was $6,934.14. Do not use the opt-out or road & bridge levy dollars in your formula.

- Take the value in line 4 ($6,934.14) times the 3.05% from line 1 to get the new base for 2025 (payable taxes). In this case, that is $6,934.14 * 3.05% ($211.491) to get $7,145.631, rounded to $7146. This is your 2025 base.

- The levy is then calculated by taking base / general levy request ($7,146) divided by the value ($38,286,484) times 1,000 (Mill Factor) to get the percentage of 0.1866.

- Mill levies are express to the third decimal point, so it will be 0.187 after rounding. The “pay 2025” general / base levy will be 0.187 per thousand which is lower than the pay 2024 base levy of 0.188 even though the township raised the base taxes by $211.

- Caveat: When I calculate the tax levies, they are then submitted to the SD-Department of Revenue (DOR) who double checks them and makes sure they comply with the laws related to property taxation.

{kind=link}